NUMBER ONE has to be TITHES & OFFERINGS. Tithes & Offerings will become the foundation that you build your house of wealth on. Without that foundation, you will lack the Ideas needed to get wealth. You will not be able to prevent the devourer from consuming your wealth. And your plans to prosper will fail. Nor will you have the power to get and keep wealth. A financial house built on a solid foundation can withstand all of the financial disasters that may come your way.

NUMBER ONE has to be TITHES & OFFERINGS. Tithes & Offerings will become the foundation that you build your house of wealth on. Without that foundation, you will lack the Ideas needed to get wealth. You will not be able to prevent the devourer from consuming your wealth. And your plans to prosper will fail. Nor will you have the power to get and keep wealth. A financial house built on a solid foundation can withstand all of the financial disasters that may come your way.

7 Ways To Increase Your Wealth

1. Create a Spending Plan & Budget If you are spending more than you earn, you will never get ahead—in fact, it’s a sure sign that your finances are headed for trouble. The best way to make sure that your income is greater than your expenses is to track your expenses for a month or two and then create a budget. It can be a very simple budget, but you should have one.

2. Pay Off Debt and Stay Out of Debt One of the best things you can do for your finances is to pay off all of your debt. To get started, focus on your most expensive debt—the credit cards and loans that charge you the highest interest. Once you have paid off all of these debts, focus on paying off your mortgage. For your mortgage, consider splitting your monthly payment in half and paying bi-weekly. Then pay extra as you can afford it. This will shave years off your mortgage and save you tens of thousands of dollars in interest.

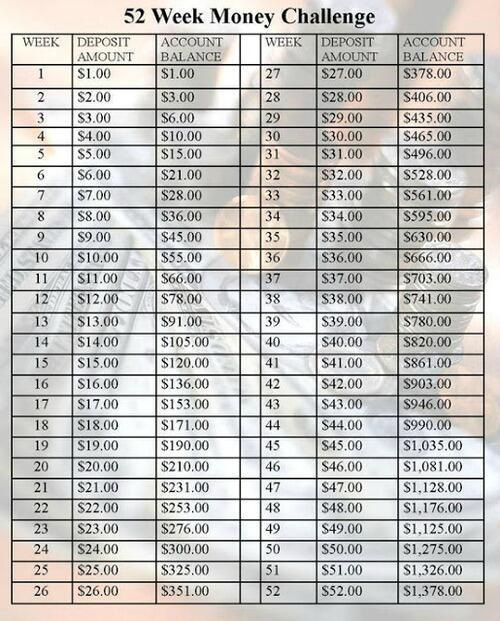

3. Prepare for the Future – Set Savings Goals Saving money for your future is crucial. If you don’t set savings goals and steadily work towards them, you will have to rely on credit when times get tough. You might even need to work through your retirement years to supplement your small government pension. Entering retirement may also be delayed or impossible if you are in debt because you need enough money to make all of your payments.

-

Start saving on a regular basis using a Tax Free Savings Account (TFSA) or an RRSP, or both (Roth or Traditional IRA Accounts)

-

Plan for your retirement. Figure out how much money you will need to retire comfortably, and then start saving. This money also makes a great rainy day fund if you lose your job or suffer another unexpected financial setback.

-

Make sure you have enough insurance. Accidents happen. 1 in 4 people get hurt on the job. Natural disasters can easily cause thousands of dollars in damage to your home. Make sure you have enough insurance for the place you live and the lifestyle you lead.

-

Write a will and decide who will get your assets and/or take care of your children when you die. This lets you decide who benefits from all of your hard work.